Healthcare M&A: Reviewing 2023 & Perspectives on 2024 H2

Healthcare Industry Insights & Outlook

The healthcare industry has shown remarkable resilience and adaptability in the face of recent economic, regulatory, and market challenges. Mergers and acquisitions (M&A) within this sector have been a significant driver of strategic growth, innovation, and consolidation. As we go into the second half of 2024, the M&A landscape in healthcare is set to experience notable shifts influenced by evolving market dynamics, technological advancements, and strategic imperatives.

Market Performance in 2023:

2023 was a tough year for dealmakers, with total M&A value dropping by 15% to $3.2 trillion, marking the lowest level in a decade. Strategic M&A1 specifically saw a 6% decline in value2.

One of the primary obstacles was the widening gap between what buyers were willing to pay and what sellers expected. This gap being further exacerbated by high interest rates and strong public markets, making private assets less attractive.

Macroeconomic uncertainty, geopolitical risks and increased regulatory scrutiny were also major headwinds, playing a significant role in slowing down deal activity. Regulatory bodies, particularly in Europe and the US, have become more vigilant, resulting in longer approval times and more conditions attached to deal completions.

Sector-Specific Trends:

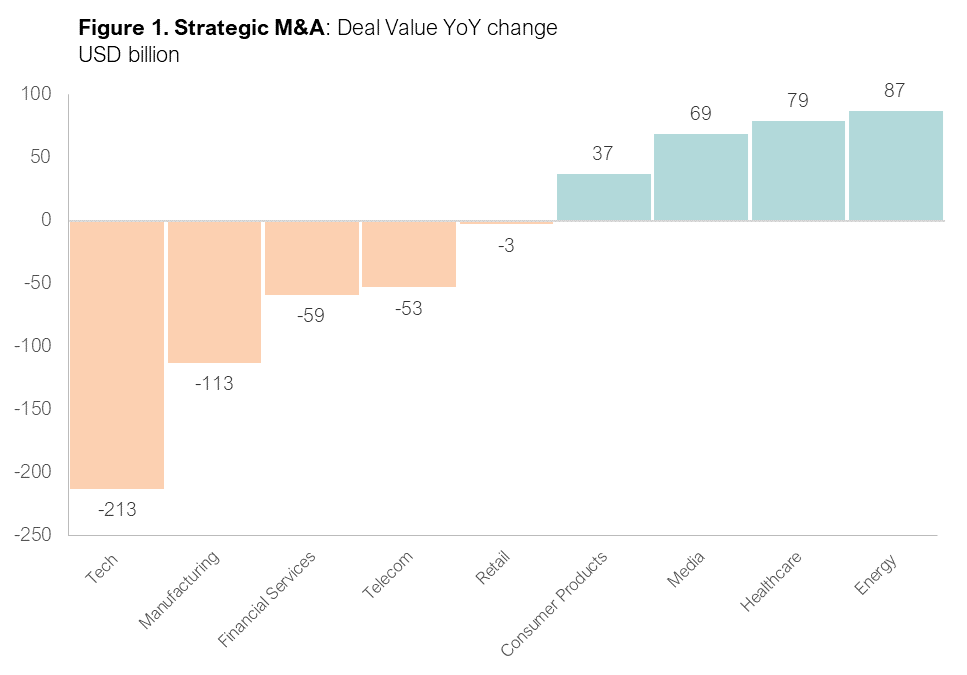

Technology deals saw the biggest decline compared to 2022, with a drop of around 43% in total deal value, largely due to the high interest rates environment impacting growth-oriented tech investments and their valuations. Manufacturing, FIG and Telecom also contributed to the slump, declining by a cumulative $228 billion year over year (figure 1).

Despite overall headwinds a select group of industries experienced a rebound in deal activity, expanding by $272 billion compared to last year.

Healthcare and life sciences standout as a sector with innovative companies attracting substantial investor interest, contributing to a 29% growth in deal volume year over year.

Healthcare and life sciences standout as a sector with innovative companies attracting substantial investor interest, contributing to a 29% growth in deal volume year over year.

Healthcare is expected to remain strong during 2024 with innovative companies attracting substantial investor interest. In this article we wanted to examine some of the industry tailwinds and hotspots for M&A activity in the coming year.

Future Outlook: H2 2024 and Beyond

An increase in dealmaking activity is expected in the second half of 2024 across the Healthcare sector as investors and lenders become more comfortable navigating the macroeconomic and regulatory environment.

Many of the assets that were held back in 2023 are expected to come to market, driven by corporates looking to divest non-core assets and private equity firms aiming to exit aging portfolio companies. There is cautious optimism about the IPO market reopening in 2024, but M&A and divestitures are expected to remain the primary exit strategies for biopharma.

Large-cap pharma companies are likely to pursue midsize biotech firms to address pipeline gaps, and private equity firms have significant funds to deploy in healthcare assets, potentially further increasing M&A activity.

A survey of healthcare industry leaders conducted by PWC finds that 54% intend to pursue M&A activities over the coming 3 years.

Corporate balance sheets remain strong, with cash reserves ready to be deployed, potentially leading to a surge in deal-making once market conditions stabilize. Big Pharma had accumulated upwards of $170 billion in cash late last year, providing plenty of dry powder for potential deals.

M&A Hotspots

In terms of which sub-verticals within the Healthcare sector might attract the attention of dealmakers we identify 4 key themes that would likely play out over the coming year and beyond.

Patent Cliffs and Pipeline Gaps: Large pharmaceutical companies are faced with impending patent cliffs, driving them to pursue acquisitions of midsize biotech firms to replenish their pipelines and sustain growth. This trend was evident as companies sought innovative targets to fill strategic gaps even throughout the market downturn.

Divestiture of Non-Core Assets: Companies will continue to divest non-core and margin-dilutive assets. This strategic move will help streamline operations, reduce R&D expenses, and generate cash to fund new investments aligned with core competencies. Such divestitures will enhance companies’ ability to pursue strategic acquisitions and drive growth. A substantial number of funds are also nearing the end of their holding periods and will contribute to the influx of assets into the market.

Digital Health and Telemedicine: The adoption of digital health technologies and telemedicine in a shift towards value-based care models will also influence M&A strategies. Companies are expected to seek capabilities that enhance remote healthcare services, with acquisitions aimed at integrating digital solutions, analytics, and telehealth capabilities will be prioritized to deliver cost-effective, patient-centric care. M&A will also be used to acquire AI capabilities that can enhance drug discovery and development processes.

Private Equity and Platform Rollups: Private equity firms will continue to focus on platform rollups in fragmented sectors such as private clinics, specialist care providers, and medtech. These sectors, characterized by operational and liquidity challenges, present opportunities for consolidation and value creation through strategic acquisitions. Companies with strong cash flows and capabilities in contract research, development, and manufacturing, might also prove attractive targets for dealmakers.

The healthcare M&A market is set for an exciting 2024 H2 ahead. With increased deal activity, driven by innovation, digital transformation, and strategic divestitures, companies have ample opportunities to achieve growth and enhance their competitive positioning. By proactively navigating regulatory challenges, leveraging technology, and focusing on long-term value creation, healthcare companies can capitalize on the dynamic M&A landscape and drive meaningful transformation in the industry.

Written by, Martin Iliev, CFO @ GlycanAge